The aviation industry plays a pivotal role in bringing people closer together. As the world’s emerging markets continue to grow, and new business models expand, aeroplane manufacturers are seeking greater diversity in their customer base.

“We know that the industries growth comes from discretionary travel and the growth of the global middle class. In an increasingly globalized and connected world, mobility is critical. The aviation industry is facilitating mobility and connectivity,” says, Boeing’s VP Sales, Marty Bentrott. While in 1994, airlines in Europe and North America carried more than 73% of all traffic, by 2034, that share will shrink to 38%, with the Asia Pacific and the Middle East airlines becoming prominent in global aviation. Each region will respond to its situations and positions accordingly with specialized requirements.

Boeing and Airbus, the world’s largest aerospace companies and leading manufacturers of commercial jetliners of defence, space and security systems, recently released a detailed forecast report on the ‘Market Outlook 2015 – 2034’ which purposes long-term forecast of passenger and cargo traffic. The report estimates the number of aeroplanes needed to support the forecast.

According to the reports, the year 2014 proved to be a successful year for the aviation industry-key metrics increased across the board and is expected to grow continuingly in the future.

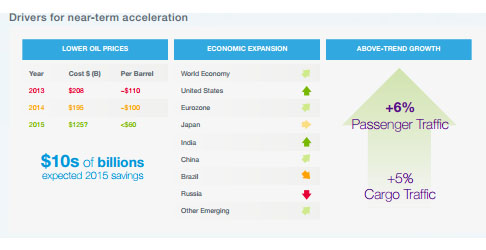

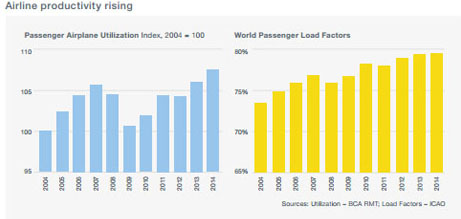

Marty Bentrott, Boeing’s Vice President Sales Middle East, Russia and Central Asia noted, “For the aviation industry, 2014 was an outstanding year. Lower oil prices saved the industry billions of dollars and airlines continued using aircraft more efficiently throughout the year. For e.g. utilization rates were 15% higher than those a decade earlier.”

Passenger traffic as measured by revenue passenger kilometres (RPK) was nearly up by 6% in 2014 and the capacity was nearly up by 5.8%. The result was recorded load factors of almost 80% worldwide. Airlines continued using their aeroplanes more efficiently, as demonstrated by utilization rates that were 15% higher than those of a decade earlier.

She added, “Because of lower oil prices and various increased efficiencies, airlines profited about US$20 billion in 2014, which was also a record year for aeroplane manufacturers. Over 1,490 jet aeroplanes were delivered and airlines ordered approximately 3,680 aeroplanes.”

The aviation industry is becoming more diverse, with approximately 40% of all new planes being delivered to airlines based in the Asia Pacific region. For the next 20 years, Boeing and Airbus have forecasted a need for 38050 aeroplanes valued at more than $5.6 trillion. An additional 20% will be delivered to airlines in Europe and North America, with the remaining 20% to be delivered to the Middle East. Latin America, the Commonwealth of the Independent States and Africa. Single-aisle aeroplanes will be commanding the largest share of new deliveries, with approximately 26730. These new aeroplanes will continue to stimulate growth for low-cost carriers and will provide needed replacements for older, less-efficient aeroplanes. In addition, wide-body fleets will need an additional 8830 new aeroplanes, which will allow airlines to serve new markets more efficiently than in the past.

“Over the next 20 years, we also forecast that the Middle East will require 3180 news aeroplanes with a market value of $730 billion by 2034,” says Boeings Sales VP Marty Bentrott.

In the past, emerging markets have driven economic growth but, Boeing and Airbus are now starting to see some regional divergence from this trend. Based on these market trends, Boeing and Airbus forecasts are an increased RPK growth to exceed by 6%, with cargo traffic growth accelerating above 5%. The bottom line is that with a favourable cost environment and strengthening demand, many airlines will see opportunities for record profits in 2015.”Global economic expansion is expected to continue with North America leading the economic acceleration and the Eurozone is finally starting to gain economic momentum.

Based on these and other market indicators, our near-team 2015 forecast is for revenue passenger kilometres (RPK) to exceed 6%, with cargo traffic growth accelerating above 5%. The bottom line is that with a favourable cost environment and strengthening demand, many airlines will see opportunities for record profits this year.”

The long-term outlook also incorporates the effects of market forces on the growth of the aviation industry. Based on this, world GDP is anticipated to grow a 3.1% annually over the next 20 years. During this time, passenger traffic is expected to grow by 4.9% and air cargo traffic by 4.7%.

The airline industry witnessed a 6% increase in passenger traffic growth last year despite weak global GDP growth. The industry continued to move forward for three consecutive years on sound fundamentals, while productivity continued to increase on historically large planesSpecifically, loading factors in 2014 improved at a considerable rate showing that airlines are matching demand without over-supplying capacity.

China and the Middle East once again led the region with double-digit traffic growth. Europe traffic grew by 5% in 2014, far outpacing economic growth, while North America’s traffic grew more than 2%. With lower fuel prices and an improving economic environment in 2015, passenger traffic is expected to once again grow at above the long-term trend.

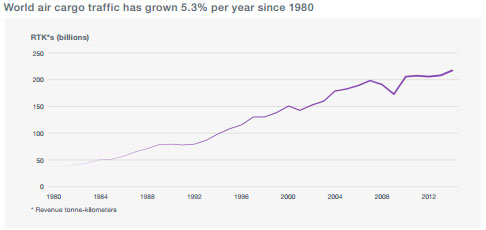

In 2014, the air cargo market was built on the recovery that began in the second quarter of 2013. Global traffic volume growth was close to the long-term average for the full year and segment profitability began to improve aided by lower oil prices. Capacity metrics also improved as utilization of large freighters returned to recent highs.

Many signals point out to global air cargo continuing to sustain on-trend growth. Global trade forecasts indicate an improving market, with trade set to grow at rates of about 5% on average over the next several years. Both are forecasted to continue increasing and will lead a return to capacity balance and profitable yields.

Industries that require transport of time-sensitive and high-value commodities such as perishables, consumer electronics, high-fashion apparel, pharmaceuticals, industrial machinery and automobile parts, recognize the unparalleled speed and reliability that air freight has to offer. These customers know the value of air freight which will continue to play a significant role in their shipping decisions.

As global GDP and world trade growth accelerate, air cargo traffic, measured in revenue tonne-kilometres, is projected to grow about 4.7% per year over the next 20 years. Replacing aged aeroplanes, plus the industry’s growth requirements will create a demand for 2340 freighter deliveries over the next 20 years. Out of these, 1420 will be passenger aeroplane conversions. The remaining 920 aeroplanes, valued at $290 billion, will be new. The overall freighter fleet will increase by more than half-from 1720 aeroplanes in 2014 to 2930 by 2034.

“In the future years, international freight is forecasted to drive overall world air cargo through 2033. World air cargo is predicted to grow at 4.7% annually over the next 20 years. Airfreight including express traffic is expected to average at a 4.8% annual growth. However, airmail traffic is said to grow much more slowly, averaging at a 1% growth through 2033.

“Asia will continue to lead the world in average annual air cargo growth with domestic. China and Intra-Asia markets will expand 6.5% to 6.7% respectively per year. Asia-North America and Europe-Asia markets will grow slightly faster than the world’s average growth rate. Latin and North America markets will grow at approximately the world average cargo rate, as well as the Middle East markets with Europe,” says Marty Bentrott, VP Sales, Boeing.

Over the next 20 years, Boeing and Airbus forecast a requirement for 1,020 standard-body freighters from converted passenger aeroplanes because of the low capital cost. Emerging markets will continue to drive strong demand. The lower purchase price of converted freighters offers carriers opportunities when high utilization and market-dependent demand are more significant considerations than performance, efficiency, and reliability. Thus, nearly 400 wide-body conversions will be needed over the forecast period.

During the forecast period, 270 medium wide-body purpose-built freighters will be delivered. Express carriers are the primary operators of medium wide-body aircraft as they possess the higher-yielding small parcel and document traffic needed to operate them more profitably. However, competition from less-expensive surface transport and passenger aeroplane lower-hold capacity constrain the use of medium widebody freighters in regional markets.

Nearly 650 new large freighters will be required where high cargo density, larger payloads and extended range are crucial.

As air travel continues to grow, airlines have a choice as to how they want to grow their business. Airlines can accommodate that growth by increasing aeroplane capacity and /or size or they can add more frequencies and non-stop markets to their networks. Passengers prefer the latter because of the increased flexibility and more efficient itineraries they offer. Adding more frequencies and non-stop services can help them fragment their existing networks.

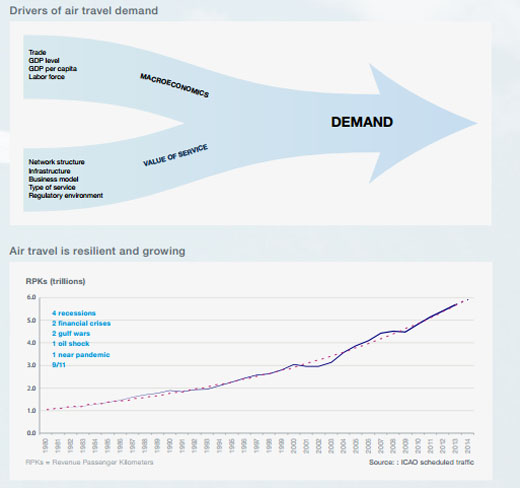

“Although the air transport industry is subjected to occasional shocks, demand is resilient, services are often seen as essential and discretionary trips such as vacations or family events are often high-priority items. Over the past 30 years, the aviation industry has experienced recessions, oil-price shocks, near pandemics, war and security threats, yet traffic has continued to grow on average at 5% annually.

This consistent growth in demand for air travel eventually leads to consistent business growth,” remarks Boeing’s, Marty Bentrott.”Air transport has been both a major driver and an indicator of the growing importance of the Middle East in the global economy. Over the past few years, Middle Eastern airlines have spear-headed growth in the region. They have extended their presence to five continents, enabling air traffic to grow twice as fast as the economy. Since 2003, capacity in terms of available seats has quadrupled to over 90 billion ASK. The Middle East is the only region in the World where the twenty-year demand for twin-aisle and Very large aircraft is greater than for single-aisle aircraft. The higher capacity of this type has been a key enabler for airline growth in the region in recent years,” Airbus spokesperson told Air Cargo Update.Recent Industry data indicate that the vast majority of growth in air travel has been met by an increase in new non-stop markets and by frequency growths and not by an increase in aeroplane capacity or size.According to Ascend online data, there were approximately 850 additional aeroplanes in commercial service in August 2014 compared with 2013, resulting in approximately 14 million additional seats for that month. The way this additional capacity was deployed illustrates that the fragmentation continues to drive market growth:

“Emerging markets throughout the world shows that air travel is one of the first discretionary expenditures to be added as consumers join the global middle class. As the emerging market demand begins to develop, it may take the form of non-scheduled services to leisure destinations. Later the same demand may migrate to scheduled services of low-fare carriers or to network airlines.

“In developed markets, demand for essential travel has been met, so growth comes from discretionary travel,” said Boeing’s Marty Bentrott.

GDP per capita matters less in these market contexts. Factors such as the availability of vacation days earned and the funds needed to travel, consumer confidence, service pricing and service quality (e.g. the availability of nonstop flights), tend to have a greater impact.

Within a given region, propensity to travel as measured in trips or in revenue passenger kilometres (RPK) generally increases with per capita income. This increase varies considerably. Generally, markets that are more open are more responsive to changes in per capita income because airlines are free to add routes, frequencies and seats to capture demand. In a more regulated environment, demand may increase with GDP per capita, but lower service quality and higher pricing may restrain travel growth. Geography may also influence travel within a region, with island geographies or poorly connected landmasses necessitating more air travel than might otherwise be the case.

Asia has become the biggest aviation market in the world and is expected to be the largest travel market to be growing at 6% annually, as a billion passengers travel to and fro every year and more than 100 billion are expected to travel in the near future. Because of this, airlines and airports in this region are expanding continually.

“One factor in this growth is the region’s GDP, which is expected to grow around 4.3% annually over the next 20 years. Although that growth will be mixed to the region’s current composition of mature, developing and emerging markets,” said Marty Bentrott.

“Whilst more developed markets will still be important, for e.g. NAM and Europe will take nearly 40% of new aircraft deliveries. The emerging

markets and the Asia-Pacific region has and will continue to grow in importance. 10 of the top 20 traffic flows forecast link passengers to the Asia Pacific, this includes the Chinese Domestic market which will become the number one traffic flow. In fact, China has increased its share of the region’s traffic from 23% in 2004 to 31% in 2014,” a spokesperson from Airbus told Air Cargo Update.

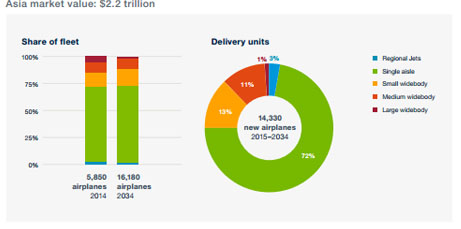

Asian GDP and passenger traffic will drive an estimated need for 14330 new aeroplanes valued at $2.2 trillion.

Meanwhile, wide-body aeroplanes such as 787 and 777 will provide the needed range and economics to open markets that were inaccessible in the past.

The 787 continues to open new markets to and from the region. Both Japan, a mature market and China, a rapidly growing market, have employed the 787 to grow long-haul share. In China, the long-haul growth rate since 2010 has been 18%, with the 787 being used primarily to open new markets. In Japan, long-haul growth has been at 9% since 2010, with more than two-thirds of its new 787s being used to open new markets. These market dynamics will lead to the regional need for 3,590 new wide-body aeroplanes by 2034.

Air cargo also plays a crucial role in Asia. The region transports a vast amount of goods over difficult terrain and vast stretches of ocean. Many of the world’s largest and most efficient cargo operators are located in the region, where the air cargo market is expected to grow by 5.7% per year. As a result, carriers in the region are expected to require 380 new production freighters and 570 converted freighters in the years ahead.

According to Airbus, the reasons why Asia will be the biggest aviation market in the future is because of:

The Middle East as a whole, is playing a pivotal role in the future of the aviation industry. The Gulf’s three biggest airlines, Emirates Airlines, Etihad Airways and Qatar Airways, are increasingly also playing an important role in the aviation industry. The favourable location of the airlines in the Middle East allows them to link many parts of the world with one-stop flights, which will help drive higher-than-average growth on those routes.

According to Boeing’s, Sales VP, Marty Bentrott, “About 80% of the world’s population lives within an eight-hour flight of the Gulf, allowing carriers in the Middle East to aggregate traffic at their hubs and offer a one-stop service between cisty pairs that would not otherwise enjoy direct itineraries.”

Technology has made the world smaller and faster.Real time communication with people from all over the world at different time zones through phones and gadgets