Asia Leads Global Air Cargo Growth as Central Asia and Gulf Regions Excel

Analysis by WorldACD highlights the highest-performing origin subregions in the first half of the year, with top-performing markets including Central Asia (+36%), the Gulf Area, and various subregions in Asia Pacific

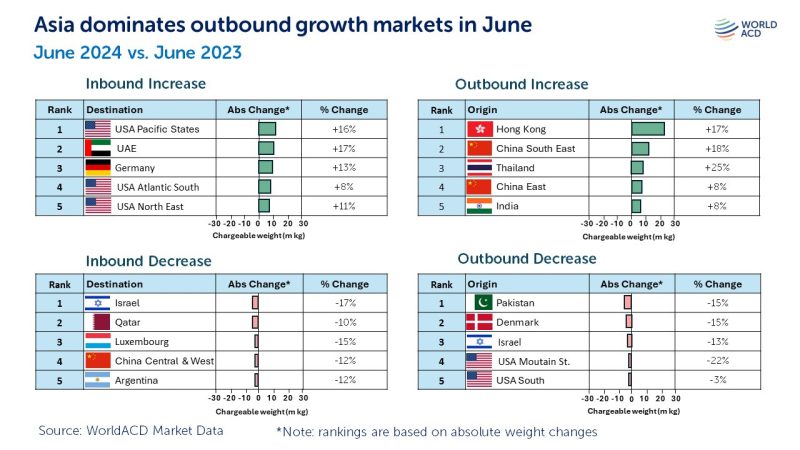

Asia currently dominates the world’s top outbound air cargo growth markets, with countries in Asia filling all of the top 5 export tonnage growth positions in June and forming most of the strongest outbound growth subregions in the first half of 2024, according to new analysis from WorldACD Market Data.

Hong Kong in June once again topped the monthly country rankings in terms of absolute increases in outbound chargeable weight flown, with an increase of nearly 23 million kgs (23,000 tonnes), compared with June 2023, a year-on-year (YoY) rise of +17% from a subregion seeing exceptionally strong growth in cross-border e-commerce traffic. It was followed by China South East with an increase of nearly 13 million kgs (+18%), Thailand (+9 million kgs, +25%), China East (+7 million kgs, +8%), and India (+7 million kgs, +8%).On the inbound side, the USA Pacific States subregion again tops the monthly rankings in June for total increases in chargeable weight, with a YoY increase of 13 million kilos (+16%), followed by the UAE (+10 million kgs, +17%), Germany (+9 million kgs, +13%), USA Atlantic South (+8 million kgs, +8%), and USA North East (+7 million kgs, +11%).

Unsurprisingly, the single country recording the biggest outbound growth has been China It recorded an increase of 30 million kgs in June, based on the more than 2 million monthly transactions covered by WorldACD’s data. For the first half (H1) of 2024, the combined outbound tonnages from China and Hong Kong rose by +24% compared with the first six month of 2023. This strong rate of YoY growth in 2024 follows a +12% YoY rise for the full year 2023. However, much of that increase last year occurred in the second half (H2) – meaning that YoY comparisons in H2 this year may show lower percentage growth numbers than those seen in H1.Weight growth by subregion:

Central Asia records +36% increase

Examining chargeable weight growth for the main global origin subregions for the first half of 2024 reveals some interesting patterns and trends, and also reinforces the message that much of the worldwide growth this year is being driven from Asian origin points, although there are some other strong growth areas.The highest percentage growth, YoY, comes from Central Asia at +36%, followed by the Gulf Area at +31%, where air cargo tonnages have been boosted by restricted container shipping capacity because of the attacks on vessels in the Red Sea. Other strong growth subregions within Asia include South Asia (+20%), South East Asia (+19%), and Northeast Asia (+16%). But there has also been strong growth in the first half of 2024 from North Africa (+22%) and the Balkan & SE Europe subregion (+22%), along with Southern Africa (+17%), Australasia & Pacific (+17%), and Eastern Europe (+12%). Subregions recording modest growth in H1 include Western Europe (+7%), South America (+6%), Canada (+5%), West Africa (+5%), and USA (+3%), with Central Africa, East Africa and Central America more or less flat.

Meanwhile, only a handful of subregions have recorded significant declines in H1, most notably Mexico (-10%), Caribbean (-10%), and Levant & Caucasus (-8%).

Half-year global growth of +12%

Analysis by WorldACD of the full global market reveals that worldwide tonnages were up by +12%, YoY, in the first half of 2024, driven by a +19% YoY increase from the big Asia Pacific origin region and a +20% rise from Middle East & South Asia (MESA) origins. Africa (+8%), Europe (+7%), Central & South America (CSA, +5%), and North America (+2%) saw more-modest YoY growth.Chargeable weight moved back into worldwide YoY growth again last October, with growth continuing since then. That follows full-year declines in 2022 and 2023 of -6% and -5%, respectively.

Average worldwide rates in the first half of 2024, based on a full-market combination of contract rates and spot rates, were -8% below their levels in the first half of 2023, with MESA the only origin region to record a YoY increase (+27%) in the first half year, due largely to the disruptions to container shipping across that region caused by the attacks on vessels in the Red Sea. However, average global prices have risen back into positive territory, YoY, since May, driven upwards by strong increases in pricing from many Asia Pacific and MESA origin points.

General cargo vs special cargo growth

As noted in the previous Trends Special report, the growth of ‘general cargo’ air freight tonnages is outpacing that of ‘special cargo’ products this year, with general cargo growing by +13%, YoY, in H1 compared with +9% for special cargo products.This reverses a trend in recent years in which demand from air cargo shipments requiring special handling, packaging, labelling and documentation has broadly outperformed general cargo. This change from the longer-term trend is mainly due to the exceptionally strong growth since last autumn in cross-border e-commerce traffic – which often flies as general cargo rather than within a special cargo handling category.

Among the special cargo product categories there has been extremely strong (+24%) YoY growth in worldwide shipments of vulnerable/high-tech cargo and in meat shipments in H1. Fruit & vegetables traffic grew by +8%, flowers by +6%, valuables and dangerous goods shipments each grew by +3%, and pharma/temp (temperature-controlled – predominantly pharma – shipments) saw a small increase (+1%). Meanwhile, fish & seafood saw a small decline (-1%), while live animal shipments dropped by -7%, and human remains by -11%, YoY, in H1.

Globally, the proportion of special cargo products within the total market averaged 35% in H1. But analysis according to the origin region of the cargo reveals some significant differences in both their ratios and their respective rates of growth. For example, general cargo makes up around 70% of the key Asia Pacific origin market, although the growth of special cargo from Asia Pacific (+23%) is higher this year than for general cargo (+17%), analysis by WorldACD reveals. In contrast, for the MESA origin market – which has been particularly impacted by disruptions to container shipping this year – general cargo growth (+28%) far outpaced the growth of special cargo (+7%).

Capacity rise of +4

Despite the usual seasonal fluctuations, the total amount of air cargo capacity available in the global market has continued to rebound, with capacity in June around +4% higher than in June 2023. An increase in widebody passenger aircraft means the proportion of cargo capacity offered by carriers operating passenger aircraft fleets has risen slightly, from 27% a year ago year to 28% in June 2024, with the proportion available in freighter aircraft operated by integrators decreasing, correspondingly, from 14% to 13%. The proportion operated by non-integrator all-cargo airlines, and by airlines operating mixed freighter and passenger aircraft fleets, has remained stable, at 10% and 50%, respectively.

Examining the performance of carrier types and the aircraft types they operate reveals significantly lower growth in the tonnages carried via freighters (+7%) in the first half of this year, compared with the equivalent period last year, whereas cargo carried via passenger aircraft (+15%) and mixed fleets (+12%) has grown more strongly.